This blog is part of Digital Health in Europe: A Data-Driven Blog Series by Speedinvest and builds on our analysis of 600+ Digital Health startups founded in Europe in the last decade.

Digital Health in DACH: A continuously thriving sector

In our previous macro analysis of the European Digital Health landscape, we found that the German-speaking countries of Austria, Germany and Switzerland (combined “DACH”) make up the region in Europe with the second largest number of startups founded between 2010 and 2020, only beaten by the UK.

102 Digital Health startups have been founded (and funded) since 2010. With about €900m of VC funding flowing into these companies, DACH ranks second in total funding behind the UK (with more than €2bn). However, with approximate €9m total funding per capita, the DACH region only ranks fourth after the UK, Northern Europe and France.

Overall startup activity in the Digital Health space has continuously increased over the years with strong acceleration since 2019. We argue this is due to three major factors:

- First, serial founders (also from other industries) or key employees from the first wave of Digital Health startups increasingly return to found their own Digital Health companies.

- Second, Digital Health is being pushed by regulatory advances, most notably the German Digital Care Act (DVG) that came into effect in 2020.

- Third, despite their traditional world-class reputation, COVID-19 has uncovered weaknesses and vulnerabilities in DACH healthcare systems. This has paved the way for the accelerated adoption of digital healthcare services.

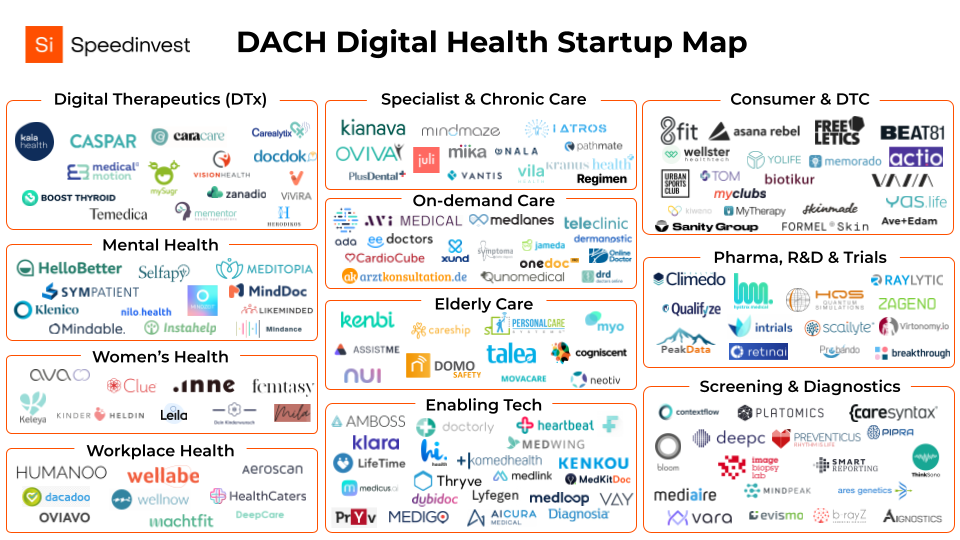

The data: 142 startups that shape the Digital Health ecosystem in the DACH region

The aim of this blog is neither to be exhaustive nor to rank startups, but rather to chart the rapidly expanding DACH Digital Health startup ecosystem. Check out our methodology blog for our inclusion/exclusion criteria. In a nutshell: We’re only including companies that build health-focused software, have some form of VC or angel funding and were founded in the last ten years.

This is the first such map that we know of and we’ll continue to expand and improve it. If your company is not on the map and you’d like to be included, please fill in this form and we’ll add you!

Let’s dive into some of the most prominent sub-verticals of the region.

Digital Therapeutics (DTx)

DACH is home to a number of successful companies focusing on musculoskeletal conditions (MSK), including mature early movers like kaia health ($26m Series A in 2020), Caspar Health (€5m Series A in 2020) and Temedica. Other mature startups in this segment often target specialized conditions. For example, Caracare treats people with chronic gastrointestinal issues and mySugr (exited to Roche in 2017) focuses on diabetes patients.

More recently, the new DVG reimbursement regime unleashed a DTx boom - particularly in Germany - by making health apps reimbursable. We share Heal Capital’s view on the many challenges this new market faces. Despite these challenges, the regulatory changes have energized the entire ecosystem. Currently, there are ten officially listed Digital Health applications (DiGAs). The full list of currently registered DiGAs can be found here. Keep checking back because dozens more are currently under review.

The currently available DiGAs include psychological use cases, such as Selfapy (depression) and Sympatient (phobias), as well as physical well-being like the treatment of musculoskeletal conditions (Vivira). There are also more specialized use cases, such as Newsenselab, which is used to treat migraines, Kalmeda, which targets tinnitus, and elevida, which supports multiple sclerosis patients.

Mental Health

We’re excited by the high number of startups targeting mental health issues in DACH. Several companies offer various forms of cognitive behavioral therapy (CBT) programs, such as Hellobetter (online courses for stress relief, sleep, to alcohol addiction), Selfapy (focus on depression) or Mindable (helps bridge the gap anxiety disorder patients face between diagnosis and treatment). Instahelp offers an online platform for psychologists. Klenico is a diagnostic support tool for mental health professionals. A number of companies also focus more on workplace mental health, including Mindance and nilo health.

Women’s Health

This segment has seen a real wave of new entrants over the past few years across Europe. In DACH, similar to the rest of Europe, the first successful companies that have raised significant amounts of money in that space were in menstrual tracking or fertility services. Clue offers B2C menstrual and ovulation tracking, both ava and inne offer hardware-enabled fertility services for women. Further down the (successful) fertility journey, Keleya and Kinderheldin have brought pre- and postnatal care online. On the leisure side, femtasy is producing female-first audio erotica and sensual stories.

Workplace Health

DACH is home to several platforms that deliver workplace health services online. All of them try to increase participation rate amongst employees and enable long-term engagement to increase ROI for companies. Humanoo, dacadoo, machtfit, wellabe and aeroscan are all playing in this large market.

Specialist & Chronic Care

Chronic disease patients are one of the biggest cost factors for healthcare systems and an attractive market for tech players. Perhaps the best-known success story is Oviva, which helps people with diabetes achieve a healthier lifestyle. iATROS supports people who need to keep their cardiovascular system under control, and mika is offering an interactive companion app for oncology patients.

Our portfolio company Kianava serves chronic patients with evidence based personalized care programs supported by a multidisciplinary team over several months.

On-demand Care

On-demand care startups give users convenience and help providers efficiently manage and triage patients.

Players in this segment include pure digital offers, such telehealth provider teleclinic (acquired by Zur Rose in 2020) and symptom checker and triaging solutions ada health, xund and symptoma. Other players make access to healthcare easier in the offline world. Avi Medical builds next-gen primary care practices in Germany, and medlanes (recently acquired by Zava Care) offers doctor home visits for acute use cases.

Elderly Care

Given the demographics of the DACH region, this segment is one expected to be of increasing importance over the decades to come. Companies in this space include communication solutions for eldery care providers, like myo care, actual home care platforms such as Kenbi or talea, remote monitoring solutions like Domo Safety, and digital companions for elderly care such as nui.care. Other companies tackle problems even one step before they become acute. Cogniscent, for example, offers early detection of neurodegenerative diseases.

Enabling Tech

Companies in this segment give healthcare providers, payers and professionals horizontal tools that facilitate their job and make health delivery more efficient and effective.

One sub-segment is SaaS products for healthcare professionals, such as our portfolio company Doctorly, who are building the next-generation of practice management software for general practitioners. Startups offering patient engagement services are Klara or Medloop.

For other sub-segments in this space, it is all about valuable health data. Companies enabling communication within the healthcare system are LifeTime or Famedly (secure messenger for HC professionals) or Komed Health (adding real-time patient data on top). Adding more actionable insights to patient vital data is done by players like Thryve Health or Kenkou, that leverage existing device data and enrich them for specific use cases. Heartbeat Medical and Lyfegen are two examples of companies that help payers, providers and pharma companies deliver value-based healthcare by capturing patient outcome data

Other notable startups in the enabling tech segment include an HR platform for healthcare professionals by Medwing and medical education scale-up AMBOSS.

Consumer & DTC

While there are numerous companies in the space and startups from other segments could be named here as well, we find that companies in this market mostly fall into two sub-categories.

First, solutions that offer services and content around topics like fitness, wellness and nutrition: 8fit, freeletics, asana rebel, Vaha, and actio belong to the key players in this area. Business models here are mostly B2C subscriptions.

The second area where we see a lot of activity is in direct-to-consumer plays among different verticals: Formel Skin (personalized skin care products), Wellster Healthtech (generic drugs for specific use cases) or Sanity Group (medical cannabis).

Pharma, R&D & Trials

We have aggregated three sub-categories into this segment, all of which touch the life science industry.

Companies that enable pharma companies on a commercial level are, for instance, PeakData (platform to identify key opinion leaders) or Qualifyze (supplier audits).

Startups that facilitate the R&D process are zageno (lab marketplace), Climedo (medical data capture), Raylytic (science platform for medical data), retinai (data intelligence platform for ophthalmology) or Breakthrough Health (RWE for MS research).

Companies that focus on recruitment for clinical trials are intrials and probando, while Virtonomy brings digital anatomical twins to clinical trials.

Screening & Diagnostics

This segment includes companies that offer diagnostic services, mostly by applying AI to medical image analysis. Companies in this space include Caresyntax (digital surgery platform), Contextflow or Deepc.ai (radiology AI platforms), mediaire (AI assistant for neuroimaging), Mindpeak or AIgnostics (pathology AI platforms), vara (breast cancer screening) or Smart Reporting (automated radiology reporting).