Now that money is on the table, you must choose from whom to take it. Here are some thoughts on what matters, drawn from personal experience.

Let me first address the why question. Why is it crucial to evaluate your follow-on investor before accepting any offer?

We are at the dawn of a unique and tough funding climate for startups. Hence the choice of investor becomes ever more important.

As a reader of this post you are probably running a fully-fledged business with employees on your payroll and a paying customer base. Another fair assumption is that your business is on an upward trajectory, where costs (e.g. hiring) are increasing at pace with your sales. Your cash runway is running its course (or maybe shortening), meaning it is again time to raise money! And here is where the need for a follow-on investor presents itself…

But you shouldn’t take just any investor on board; your follow-on investors ought to be great. With their advice and connections, they can facilitate the step change you need to go from a good product-market fit to a fast-growing business machine. The valuation they put on your company can dictate your media attention and how you are viewed by future investors. The deal terms they ask for can directly affect your cap table attractiveness, which, in turn, could be the dealbreaker in your next funding round and possibly even the timing of your exit. Your investors’ vision for your company will completely change its trajectory.

Worst case scenario, your follow-on investor could be debilitating by pausing your growth or vetoing strategic decisions. They could even kick you out of your business if you give out too much power. Given the size and breadth of our portfolio of 100+ companies, Speedinvest has already seen pretty much each and every scenario play out. When Atomico invested in Bitmovin, that was a game changer. For another one of our portfolio companies, Tourradar, it was Hoxton Ventures’ and Cherry Ventures’ global fundraising know-how which made all the difference, enabling them to grow to become one of the top eCommerce players in Europe.

Follow-on investors will examine you through a lens of rigorous fund management, experience and expertise in the field and with a team who will assess you on your numbers. So it’s only fair to assess your investors with the same rigor.

But how can you find out whether a potential investor will be a great follow-on investor? To start out, I would bucket my criteria into three categories covering a set of business, legal and interpersonal topics:

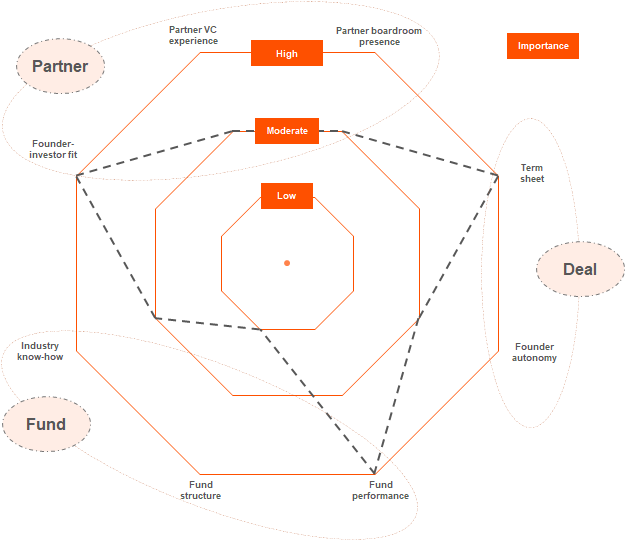

- The Firm (aka Signaling & Investor/Company Fit)

- The Partner/Founder Relationship

- The Deal

What kind of firm will I be working with?

So what is the profile of a typical follow-on investor? Here no single rule applies, but in broad terms they have deeper pockets than your last investor in order to be able to participate in more rounds (exercising their pro-rata rights). With this characteristic in mind it becomes obvious that your follow-on investor will (with some exceptions) be an institution. And similar to your own company, every institution comes with its own structures, rules and protocols that you should know.

Fund structure

A VC is not a typical company. After a couple of explainers on how VC works, you should by now get what a fund is and how its business model works, including fund lifetime. There is a fund structure, as well as what they call fiduciary responsibilities. Yet again, they will hardly ever bother you with specifics. That does not mean that any of this stuff cannot influence your business in the long run.

To put it plainly, the fresher, the better. If a VC has raised money very recently, they have a greater availability of capital and more time to invest and reinvest. Still, size does not trump everything. The more companies they have in their portfolio, the less significance your company will have in their portfolio. It is a trade-off if they do not expand their own team, thereby strengthening the firm’s deal sourcing, due diligence and portfolio monitoring capabilities. Think of three axes: portfolio size, team capabilities and time since fund vintage. One can rarely optimize for all three at the same time, so try your best on at least two.

Industry know-how

A follow-on investor’s quality of resources is also influenced by its approach towards investing (more passive or more active) and the depth of expertise in your field. The advisory role of an investor is a confluence between the firm’s human capital (e.g. experience) and intellectual capital, ie. their collective memory of decisions leading to certain outcomes.

On the one hand, you want your investor to offer you informed, data-driven company-specific advice. Yet on the other hand, you also want on your side an institution that has seen things go sour before, so they can warn you in time to steer your company’s ship in another direction.

Fund performance

Best proof of an investor’s quality, in a game with incomplete information like fundraising, are tangible results. Since you can’t predict the future, the next best thing is the fund’s past performance. That is relatively easy to find. Similar to other fields of finance, household names in VC are top-performing and well-run institutions. In our industry, brand is cultivated by reputation, media attention and other forms of publicity. In turn, media attention comes with million-dollar exits and unicorn valuation rounds. Another proxy for performance are any co-investors that the firm has partnered with, i.e. network determines reputation (and vice versa). The benefits of your investors’ networks are many and varied, including the introduction to other potential follow-on investors or strategic partners.

Finally, what is a well-run institution? This refers to how investment decisions are made and the internal power dynamics. Later, I will touch upon this by stressing the significance of your Partner’s role within her own firm. Important factors here: are decisions made in a majoritarian, consensus or veto system? How fast or slow is the process? A couple of questions never hurt.

Operational support

These days many firms will offer operational support aka platforms, to support you with specific tasks of everyday startup life. From hiring to growth and business development, the range of services might differ and also the mileage may vary. While some firms offer top-level executives on call for certain topics, other funds will dedicate hands-on resources to really get stuff done. It very much depends on your needs and what you prefer.

What kind of person will my dedicated investor Partner be?

You probably know already that when a fund invests in your company, you usually have one dedicated Partner and her team that follows your progress over the course of their investment period before exit. This is the person who will advocate for your company within the fund and make sure you get the (human and financial) resources you need. So forming a strong and meaningful relationship with her from the beginning is key. It is not mere coincidence that they are called Partners 😉. A VC is a people business, so it is crucial that you get along well.

Founder-investor fit

Choosing an investment Partner is best viewed as a business choice. And as with a business partner choice, interpersonal dynamics play a role. Ideally, you have developed good chemistry between you and the Partner. Chemistry can be attributed to a fit or appreciation of each other’s identity (culture or educational/professional background). Cultural fit is a matter of luck, but cultural appreciation is trained, just like your IQ. Whatever the source, chemistry is not built over time, but can be deepened on the way. It is all about those first interactions (ideally long before you actually go out fundraising). In the intervening months between first and follow-on round, you should have been fortunate to have tested your relationship with the Partner. Hopefully, you have by now determined whether there is real chemistry. This also shows how important it is to start building relations with potential investors as soon as possible.

Partner boardroom presence

Still, occasional phone updates are not the crux of your interactions with a Partner — boardroom discussions are much more important. They are formal, strategic and in front of others. You want her to be active in those meetings. I would call this trait ‘the Partner’s commitment to your start-up’. A busy Partner could end up sending a firm representative and the board meeting could easily be steered in a direction you do not wish to go. The representative, who could be either junior or senior, could be a fintech expert in a D2C apparel company board with no previous operational experiences to draw from. Just imagine what she has to say and what value her interventions have. Such a scenario could waste your precious time and probably irritate your other investors.

Partner VC experience

However, this is not as bad as a Partner who has not done her homework on your company. Of course, the input and knowledge of your Partner is as important in conducting her Board Member role. It is true that you can make do with Partners who do not have a doctorate in your field or have not worked in the industry for 25 years. Yet it is also valid to expect a Partner, who you ask to be your mentor/investor, to have confidence in what she advises you on. To evaluate her, observe her fluency in technicals and her inquiries about metrics and milestones that your business may be hitting. This applies to every industry, whether technical in nature or not.

Other things to look out for are her experience in VC and how senior she is in the investment firm. The VC world is dominated by its own lingo and at times feels like a cult, so an experienced pair of hands who will help to explain and navigate is in demand. You want a person old and senior enough for her opinion to matter, but also one who you can converse with and who has not detached herself from the everyday realities of running a small business. For that, you need references to come with the title and LinkedIn profile. Ask people you trust about her, because their attitude could not match what is on paper.

What are the deal mechanics to look out for?

Finally, we ought to address the big elephant in the room — the deal itself. The key here is the following: keep your eyes open and read the term sheet closely. You do not want any last minute surprises.

Term sheet

As a founder, it is a top priority to be careful who to take on your cap table. Connected to this are the clauses which were agreed upon in your previous round. In order to safeguard your ownership and control of the company in the future, what is negotiated in this round’s term sheet is critical. ‘Ratchet’ is more often than not brought to the table in contract negotiations with follow-on investors (either to exercise it or to introduce it). Here is why you may want to run away from it or limit the cases where it is exercised.

Similarly, your follow-on investors may ask to insert performance clauses, whereby a portion of the capital they are committing is unlocked after you hit certain predetermined KPIs or goals. Let me remind you, we live in a post-series state of affairs. From their perspective, this acts as an incentive mechanism to induce you and your team to work harder for earlier results. The question is whether you believe that these goals are realistic, while appropriately aligning investor/founder incentives.

Next is valuation. Be smart about it. Think big and extend your horizon beyond the 1–2 runway after this funding round is concluded. VC funding is a repeated game, where increased valuation sends positive signals about your company performance, but can also doom you for a down round with negative repercussions on your image in the media.

Founder autonomy

Other points on deal terms have been covered by my previous blog post. If I were to underline something I may not have mentioned in the past, it is voting rights. Above all, it is achieved by letting founders have control in their own companies. Alignment of investor/founder interests is ensured by not diluting the latter away or proposing vesting. Handing out extra voting rights to follow-on investors can be as risky as handing out shares.

Beyond voting rights, the constitution which governs (and possibly restricts) the running of your business should be viewed as an issue of founder autonomy. The list of actions that have to be approved by the board, e.g. if you have to approve any budget variation of 10% or any hire above 60k annually, will influence your day-to-day business. It not only slows down your decision-making operationally, it is in effect virtually handing over control to a committee of people whose interest in the company is collectively a minority. Oversight and control are two different words for a reason. The breadth of actions described in your company’s constitution draws the line between the two.

Conclusion

Having been an entrepreneur myself in some pretty nasty situations and having seen a lot of ugly stuff happening with investors, I most definitely erred towards the stuff you need to be careful about, while still being optimistic about the prospect of adding investors to the cap table. In my experience, the European VC world is overall a friendly ecosystem. Just reciprocate the exhaustive due diligence your prospective investors do on your company, as you are not the only buyer in this transaction. For those wanting to raise for the first time, a very similar process of two-sided due diligence applies.

Below is a sample graphical representation of what importance you and your team could place on each of the criteria mentioned above: