We’re one of Europe’s most active pre-seed and seed investors in Digital Health. Check out our full analysis of 600+ Digital Health startups founded in Europe in the last decade and our overviews of the Digital Health ecosystems in France and DACH.

It’s still early days for the Digital Health startup ecosystem in Europe, but we’re moving fast. When we published the first ever overview of Digital Health Exits in Europe in November 2020, we counted 22 exits ever in Europe up to that point and concluded that more happened in 2 years than the 8 years prior.

4 months later, at the end of Q1 2021, that number is 37 -- a 68% increase. This pace of change is why we’re updating our analysis in real time.

Only ~1% of startups ever exit, but exits are key moments for founders, investors and the entire startup ecosystem. They provide liquidity, release talented individuals who will start new ventures, and make the sector more attractive for investors. In a young ecosystem, exits matter even more.

Key findings we’ll share below:

- Over the last decade, there have been 37 publicly disclosed acquisitions in Digital Health in Europe.

- 17 exits (46%) occurred since the beginning of COVID-19 in 2020

- All exits to date have been M&A, there have been no IPOs

- 50% of acquisitions are by Digital Health companies

- Germany leads with 10 exited startups ahead of UK and Sweden with 5

Here’s a visualization of all the exits we count to date, include the startup, acquirer and known details of the transactions.

Of these, 17 exits happened in the last 5 quarters alone:

And here’s a year-by-year exit count:

Three high-level observations from our last analysis still apply:

- This is an extremely low number. In the US, more than 63 Digital Health exits happened in Q1-3 of 2020 alone. That’s 1.7 times Europe’s exit activity from the entire last decade.

- All transactions are private M&A with confidential terms, which makes it hard to benchmark exit valuations.

- European Digital Health founders have been eager to exit quickly, but for fairly small returns. We expect this to change.

One observation from last time needed updating

- All startups that exited (except Aurora Health) were founded from 2011–2015. Speed to exit is accelerating: 51% of startups exit in less than 5 years. More analysis below!

Where in Europe do exited Digital Health companies come from?

Interestingly, although the UK leads Europe by overall company formation and investment in Digital Health, Germany is the clear #1 source of exited Digital Health startups.

Exit targets: telemedicine, enabling tech and mental health

The chart below shows that on-demand telemedicine, enabling tech and mental health startups have been the most popular exit targets, representing more than two thirds of all exits. In our last post, mental health had still been the #1 category with 6 exits.

The biggest increase in exit activity has been driven by an ongoing consolidation in on-demand telemedicine. Telemedical providers have bought backend solutions, like Vi Health (acquired by Numan), Sprechstunde.online (acquired by Zava) or Doctorlink (acquired by Health Hero), as well as independent on-demand platforms like MedHelp (acquired by KRY) and Fernarzt (acquired by Health Hero). This extends a trend of prior acquisitions of telemedical providers like Teleclinic in Germany and Mes Docteurs in France.

Time to exit: 5 years

The average time to exit for a Digital Health company in Europe is 6.4 years, the median time to exit is five years, a slight acceleration compared to our prior analysis.

For context, a quick comparison below shows that these are slightly shorter paths to exit relative to other startups.

In our experience, Digital Health founders generally exit at the first opportunity that presents itself. VCs may frown at this, but in an immature market, as our partner Daniel Keiper-Knorr has argued before, even smaller exits can be life-changing and huge learning experiences for founders. Given how few breakout Digital Health cases we’ve seen in Europe to date, we understand that founders have doubts about longer-term growth options.

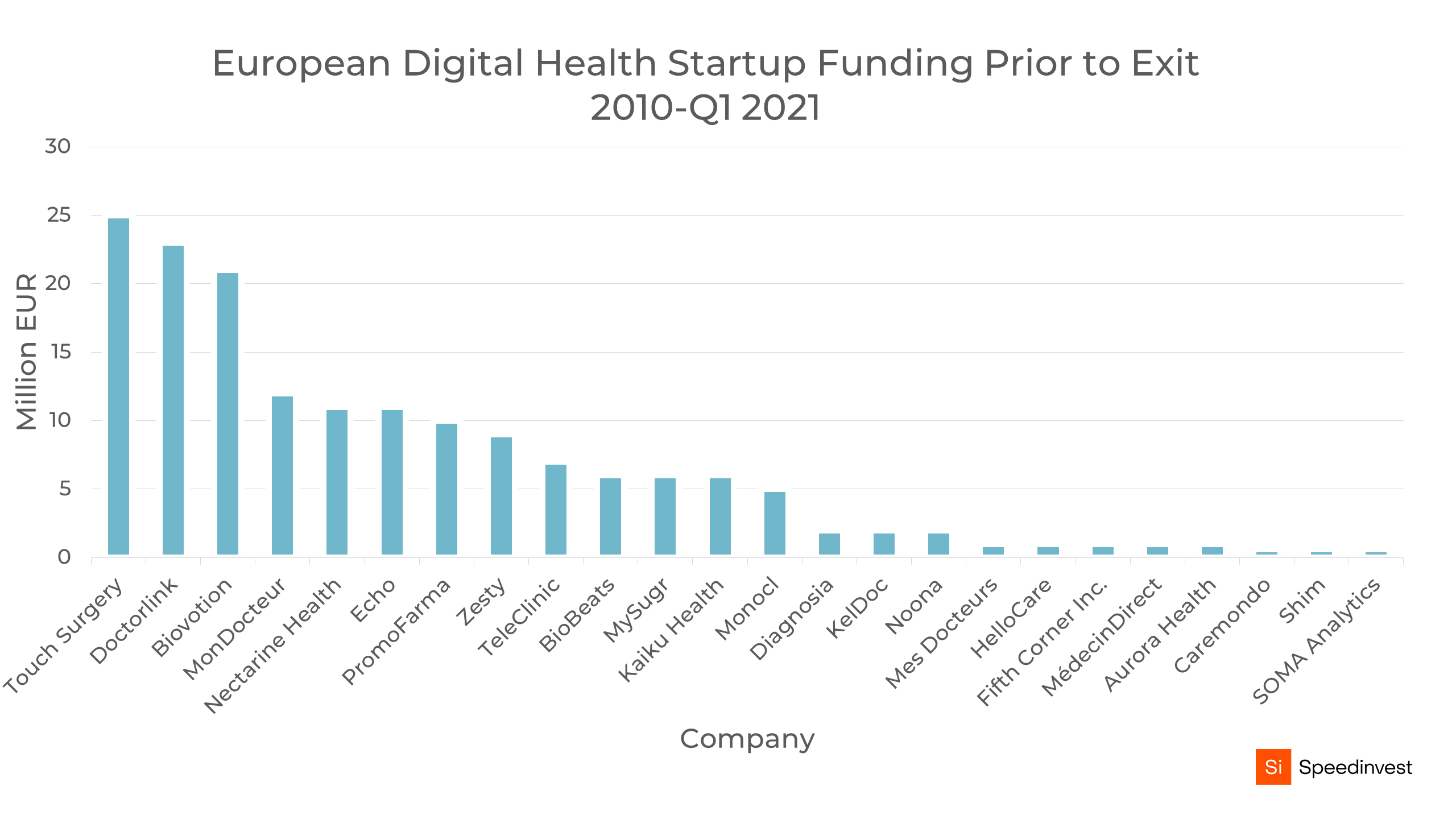

Funding until exit: low, but growing

European Digital Health companies don’t always raise a lot of money before they exit:

- Only 3 companies have raised above €20 million prior to exit (Touch Surgery, Doctorlink, Biovotion).

- Only 7 startups raised more than €10 million before getting acquired.

- Average funding (where we can access this data) is at €7m, which is broadly in line with the overall European data we analyzed in our deep dive into 600+ European Digital Health startups.

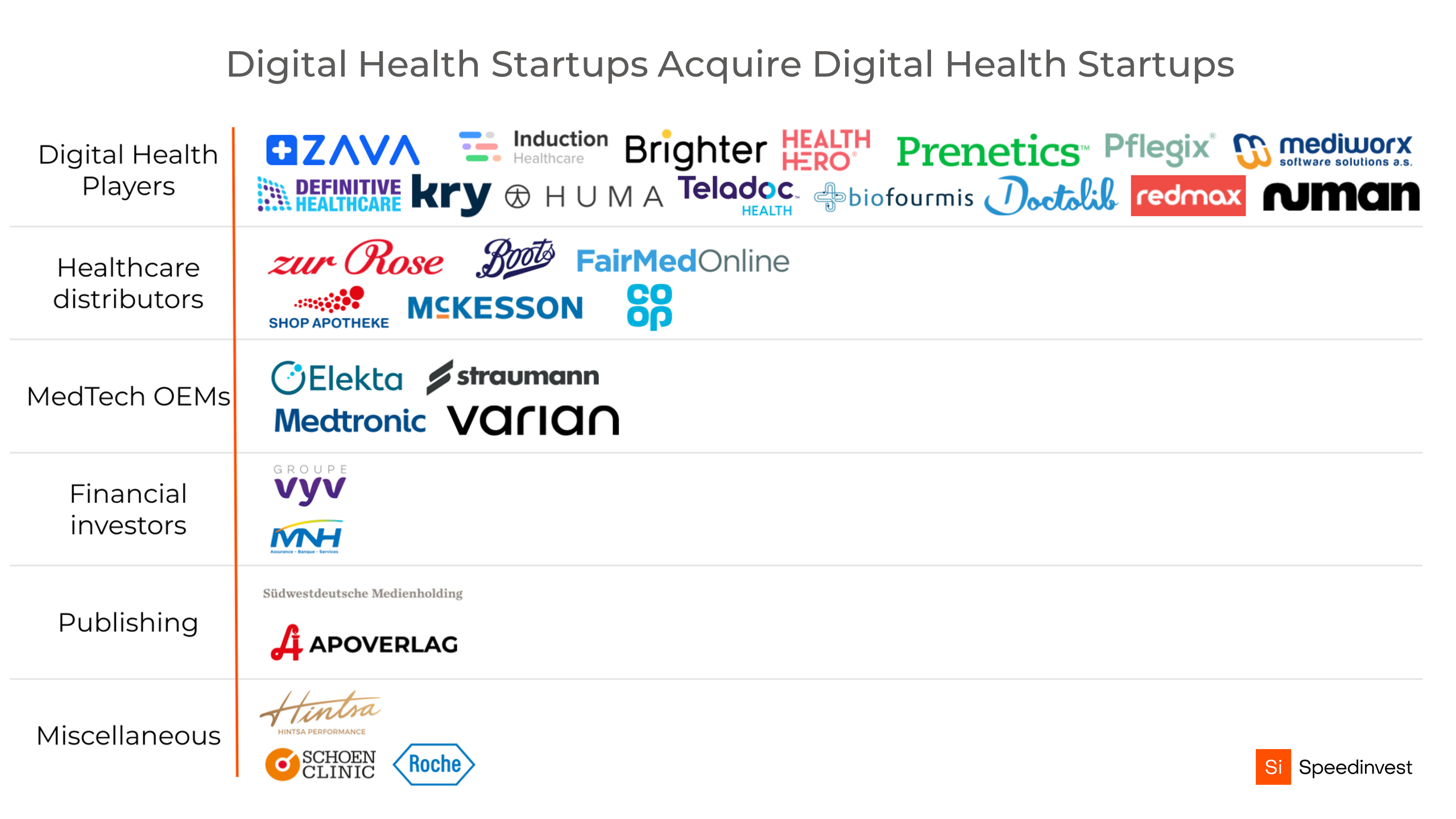

Acquirers

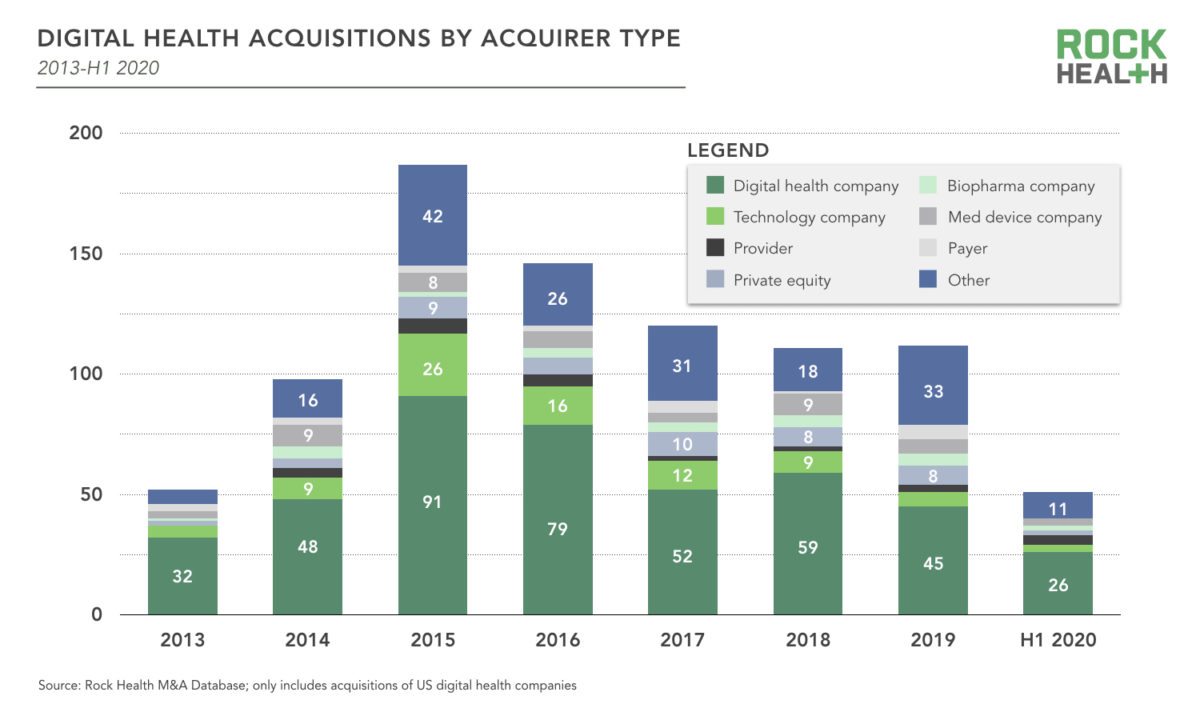

So, who is buying Digital Health startups? As a benchmark, here’s the US landscape taken from Rock Health’s summary of the US exit market.

Both in the US and Europe, Digital Health companies are the biggest acquirers of Digital Health companies, accounting for over 50% of exits, followed by pharma distributors and a mix of other strategic players:

And here’s an overview of which companies have been buying:

This pattern mirrors general trends in the software industry and is the reason why successful Digital Health companies are a benefit to the wider ecosystem; they’re major sources of capital and M&A activity. As more companies mature in this space, we also expect M&A activity to heat up.

Most recent acquisitions were driven by a buy-and-build strategy, as Digital Health scale-ups seek to expand their offering by acquiring proprietary tech and new client segments. Examples include

- Most recently, men’s health platform Numan acquiring Vi Health, a Swedish Class 1 medical device and symptom checker;

- Boston-based Biofourmis’ decision to complement its analytics platform by acquiring swiss wearable company Biovotion;

- Swedish KRY’s acquisitions of Shim, MedHelp or MJog;

- Zava’s effort to build out its telemedicine platform with acquisitions of Sprechstunde.online and Medlanes.

- Health Hero’s PE-backed roll-up of Fernarzt and Doctorlink, backed by the investment firm Marcol is driving the roll-up.

Similar to the US exit market, a large portion of exit activity is driven by a broad mix of commercial players. Some patterns we see here are:

- Healthcare distributors -- both wholesale and retail -- making strategic acquisitions to expand distribution channels or extend value chains towards end users, such as pharmacy group Zur Rose’s acquisition of Teleclinic, which makes sense given that 50% of consultations performed on Teleclinic’s platform result in electronic prescriptions;

- MedTech OEMs -- like Straumann, Varian or Medtronic -- buying access to end users (Straumann’s acquisition of Dr Smile) as well as proprietary IP and tech. In theory, these are natural acquirers for Digital Health startups. In practice, this type of deal is rare both in Europe and the US. In one of only three M&A deals in Europe, Medtronic, the largest medical device supplier in the world, acquired Touch Surgery, complementing a large portfolio of surgically implantable medical devices with a high-tech surgical training provider.

A first glimpse of 2021: Digital Health exits picking up along with funding and company formation

In our first exits article said that it’s an exciting time for Digital Health startups in Europe, that the sector is nascent, but growing fast.

Healthy and repeatable exit routes are only just emerging and will help drive founder rewards and investor returns. As more European Digital Health companies reach scale and build a stronger M&A appetite of their own (think of recent funding rounds by KRY, Doctolib, Babylon), we think the flywheel is only just beginning to turn.

We hope you’ve found this article useful. We’ll update it towards EOY 2021, or before if things heat up quickly.